The Always-Late Fed

Why the Federal Reserve’s dual mandate forces policymakers to react to recessions instead of anticipating them

Next week, on March 18, the Federal Reserve will announce its latest policy decision following the FOMC meeting.

If market pricing is correct, the decision will be straightforward: no rate cut.

According to the CME FedWatch Tool, markets currently expect the Federal Reserve to leave rates unchanged. In many ways, that outcome would not be surprising. Policymakers tend to follow market expectations closely, particularly when the consensus becomes as clear as it is now.

Yet there is something uncomfortable about this moment.

Because if one looks beyond the surface of financial markets and instead examines the underlying momentum of the business cycle, the current policy stance begins to look increasingly questionable. The signals emerging across the economy suggest that the slowdown may already be further advanced than many policymakers realize.

And that is precisely where the historical pattern becomes important.

Again and again, central banks have tended to respond after the cycle has already turned, not before. The indicators embedded in the Federal Reserve’s mandate - inflation and employment - often confirm economic turning points only after the loss of momentum is already underway.

Which raises a crucial question as the March FOMC meeting approaches:

Is the Federal Reserve once again reacting to the economy that existed months ago - rather than the one that exists today?

In this article, we will examine why this pattern occurs, why it is embedded in the structure of the Fed’s mandate, and why policy responses so often appear to arrive only after the economic cycle has already shifted.

The January 2008 “Oh No” Moment

In October 2007, the Federal Reserve did not believe the U.S. economy was heading toward a crisis.

Inside the Federal Open Market Committee (FOMC), policymakers were still primarily focused on inflation risks. The housing downturn was acknowledged, but many officials believed the broader economy would remain resilient. Growth, while slowing, was expected to continue. The financial system appeared under pressure but far from collapse.

Through the final months of 2007, the dominant concern inside the Fed was not an imminent recession - it was whether inflation might remain too high.

Then something remarkable happened.

On January 22, 2008, the Federal Reserve made an emergency decision between scheduled meetings to slash interest rates by 75 basis points. For an institution known for gradual, carefully signaled policy moves, such an inter‑meeting cut was extraordinary.

Just eight days later, at the scheduled FOMC meeting on January 30, the Fed cut rates again - another 50 basis points. In the span of a single week, the central bank had reduced the federal funds rate by 125 basis points.

To observers, the shift was dramatic. The institution that had appeared relatively calm about the economic outlook only weeks earlier was now acting with urgency.

Financial markets interpreted the move as a signal that conditions had deteriorated rapidly.

But this raises an important question. Did the largest economy in the world truly collapse in the span of a few weeks?

Economic systems rarely behave like that. The U.S. economy is an enormous and complex structure composed of millions of households, businesses, and financial institutions.

Such systems do not suddenly reverse direction overnight.

Instead, they lose momentum gradually.

Housing activity weakens. Consumer confidence deteriorates. Credit conditions tighten. Job creation slows. These developments often unfold over many months before they become visible in the official indicators policymakers rely upon.

By the time the Federal Reserve executed its emergency cuts in January 2008, many of these signals had already been building for some time. The sudden urgency was not the result of a sudden economic collapse. It was the moment when policymakers finally recognized that the cycle had already begun to turn.

And this pattern - apparent stability followed by sudden policy panic - has repeated itself more than once in modern economic history.

Large Systems Do Not Turn Suddenly

If the emergency actions of January 2008 were truly caused by a sudden collapse in economic conditions, it would imply something rather unusual about how economies function.

It would mean that the largest and most complex economic system in the world can change direction almost instantly. History suggests the opposite.

Large systems rarely move abruptly. They change direction gradually because they possess inertia. In physics, massive objects do not suddenly stop or reverse course. Momentum slows first. Only after the deceleration becomes strong enough does the direction finally change. Economies behave in a remarkably similar way.

The U.S. economy is an enormous network of households, businesses, financial institutions, and credit relationships. Consumption decisions, hiring plans, investment projects, and lending activity unfold over months and years. When momentum in such a system begins to weaken, it typically does so progressively rather than instantaneously.

Early in the process, the changes are subtle. Housing activity begins to soften. Credit conditions tighten slightly. Consumers become more cautious with spending. Businesses slow the pace of hiring. None of these developments, on their own, immediately signal recession. But together they reflect something more important: the gradual loss of economic momentum.

Only later do the widely followed indicators begin to deteriorate.

Unemployment rises after companies reduce hiring or initiate layoffs. Inflation falls only after demand weakens and pricing pressures subside. By the time these indicators clearly signal trouble, the economy has often already been slowing for some time.

This difference between momentum and confirmation is central to understanding the business cycle.

Turning points in the economy rarely begin with dramatic events. They begin with a gradual deceleration that spreads through the system. Housing weakens, consumer confidence fades, credit becomes more restrictive, and job creation slows. These shifts represent the early loss of momentum that precedes broader downturns.

Yet the indicators most closely watched by policymakers often capture the cycle only after these developments are well underway. This creates the appearance that economic downturns arrive suddenly. In reality, the slowdown has usually been developing beneath the surface for months before it becomes obvious.

Understanding this distinction between momentum and confirmation is essential for interpreting the behavior of central banks - and for understanding why policy responses so often appear to come too late.

The Fed’s Dual Mandate

To understand why the Federal Reserve so often appears late in responding to economic turning points, it is necessary to examine the framework under which it operates.

The Federal Reserve does not simply set monetary policy based on its own judgment of the economy. Its objectives are defined by Congress through what is known as the central bank’s dual mandate. Policymakers are tasked with pursuing two goals simultaneously: stable prices and maximum employment.

At first glance, the mandate appears straightforward. A central bank should aim to keep inflation low while ensuring that the labor market remains strong. These goals sound both reasonable and complementary. In practice, however, the structure of the mandate creates a fundamental timing challenge.

Employment is a Coincident indicator – whereas inflation is a Lagging indicator of the business cycle.

Inflation typically rises during the later stages of economic expansions – and even into the slowdown and the Recession. Strong demand allows companies to raise prices, and tight labor markets put upward pressure on wages. These forces accumulate over time, which means that inflation often peaks just as economic momentum is beginning to slow.

Employment follows a similar pattern. Companies rarely react immediately to weakening demand. Instead, businesses typically slow hiring first, reduce working hours, and only later begin layoffs. As a result, the labor market often appears resilient even as the broader economy in the initial phases of a slowdown is losing momentum.

This dynamic creates a dilemma for policymakers.

If the Federal Reserve waits for inflation to fall back toward its target before easing policy, it risks maintaining tight financial conditions precisely when the economy is already weakening. If it waits for unemployment to rise before responding, the slowdown may already be well underway.

In other words, the indicators embedded in the Fed’s mandate tend to confirm economic turning points after they have already occurred.

This is not a criticism of policymakers themselves. Central banks are designed to be cautious institutions. Acting too early carries its own risks. If the Fed cuts interest rates prematurely and inflation returns, it can damage the credibility that monetary authorities rely on to anchor expectations.

As a result, policymakers often prefer to wait for clearer confirmation in the data before making large policy shifts. But that caution comes with a cost.

By the time inflation is clearly declining or the labor market visibly deteriorates, the underlying momentum of the economy may already have changed. The turning point of the cycle has already occurred - only the confirmation arrives later.

This structural feature of the dual mandate helps explain why monetary policy so often appears reactive rather than anticipatory. The Federal Reserve is not simply trying to predict the future of the economy; it is responding to indicators that were never designed to provide early warnings in the first place.

Inflation - The First Trap

One of the most persistent misconceptions in economic policy is the belief that inflation provides an early signal about the state of the economy.

In reality, inflation is one of the most Lagging indicators in the entire business cycle.

Price pressures typically build during the later stages of an expansion. As demand strengthens and labor markets tighten, companies gain the ability to raise prices and wages begin to accelerate. These developments accumulate slowly over time, which means inflation often reaches its peak just as the underlying momentum of the economy is already beginning to weaken.

This creates a difficult dilemma for central banks.

If policymakers focus primarily on inflation levels when determining policy, they may be responding to conditions that reflect the **past phase of the cycle rather than the current one**. By the time inflation becomes clearly elevated, the forces that produced it - strong growth, tight labor markets, and robust demand - may already be fading.

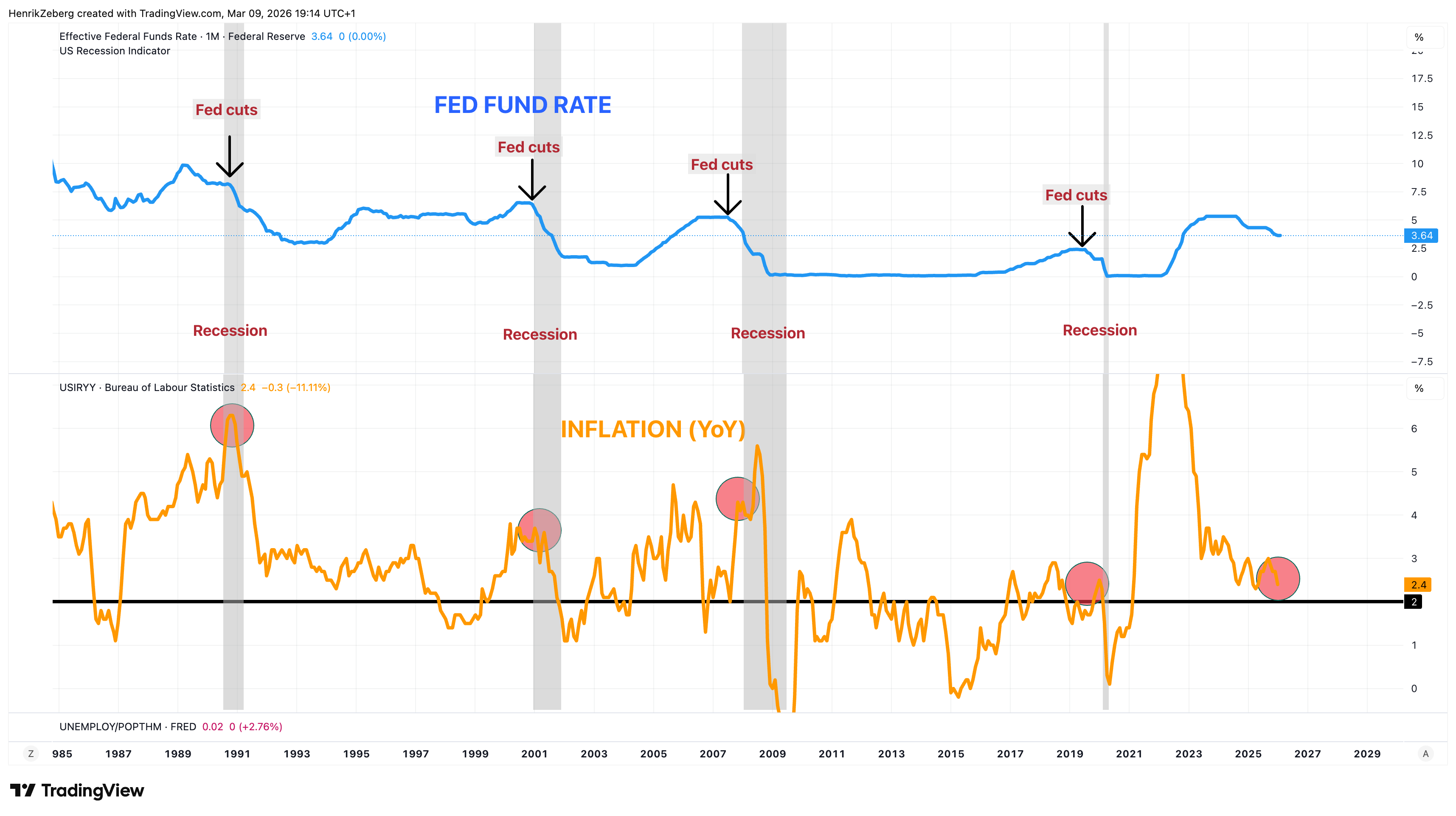

History shows this pattern repeatedly. During several past economic cycles, inflation remained elevated even as the broader economy was losing momentum. Policymakers, concerned about price stability, hesitated to ease policy while inflation was still above target. Yet by the time inflation eventually began to decline, the slowdown in economic activity was already well underway. This dynamic is clearly visible in the historical relationship between the Federal Funds Rate and inflation.

Chart: Federal Funds Rate vs. Inflation (with U.S. recessions highlighted)

The chart illustrates a striking pattern across multiple decades of economic cycles. In several instances, the Federal Reserve began cutting interest rates while inflation was still elevated or even rising. At first glance, this appears counterintuitive. If the central bank’s mandate emphasizes price stability, why would it ease policy while inflation remains high?