The Quiet Hand

Why the most exuberant market in history is standing on an economy that is already rolling over - and why nobody whose job it is to see it, can.

I. An invitation, and a door held shut

Earlier this year I was invited to give a keynote. A large conference, several hundred people in the room, the kind of high-profile stage where you are asked to stand up and tell an audience what you actually think. I had my talk built in my head before I finished reading the email. Three parts.

First: why the financial industry did not see the 2008 recession coming - and, from the opposite end, why it got 2022 wrong too. Second: how the Macro Navigation Framework™ actually forecasts recessions, and how any investor can use the four phases of the business cycle to position ahead of the turn instead of behind it. Third: a live, real-time picture of exactly how close the United States is, right now, to falling into recession.

The reply, when it came, was a single sentence dressed as politeness:

“We can perhaps follow up later in the year, I will keep you in mind if

investor concerns around a potential US recession become more acute.”

I will be honest about my first reaction, because there is no point pretending otherwise. I was disappointed. You build something over years, you test it across half a century of data, and a stranger closes the door in a sentence.

And then, somewhere in the second cup of coffee, the disappointment turned into something more useful. Because that sentence - that exact, well-mannered, utterly complacent sentence - is the thesis. It is the single cleanest illustration I have ever been handed of why the Macro Navigation Framework needs to exist at all. So let me take it apart, slowly, in public, with the data. And then let me leave a record - this article - that you and I can both return to in six or twelve months and check against reality.

II. The 6% that should end the argument

Let me start with the gatekeeper’s own instrument. He will act “if investor concerns become more acute.” Fine. Let us look at investor concern - the actual, measurable probability the market assigns to a US recession - and let us look at what it did the last time the house was on fire.

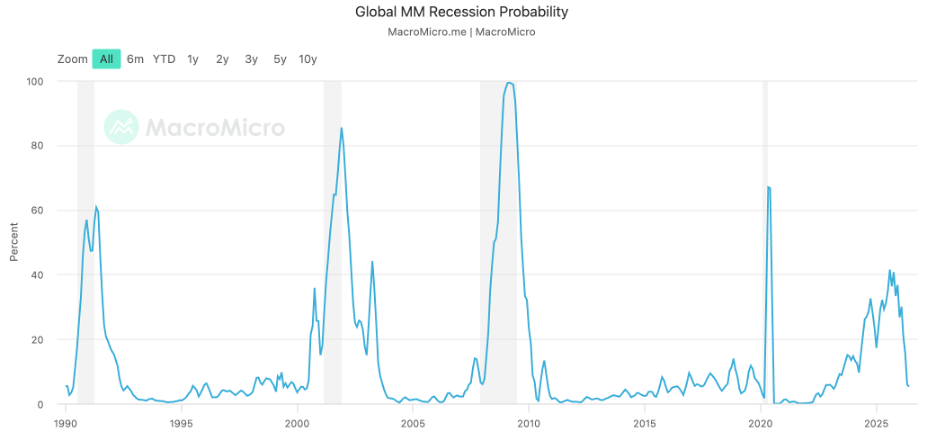

Global recession probability (MacroMicro). Note the reading going into each recession - and where it sits today.

In December 2007 - the first month of what became the Global Financial Crisis recession - this probability read 6%. Six. By March 2008, with the recession already four months old and the labour market visibly buckling, it had climbed all the way to 14%. The spike to near-certainty did not arrive until 2009, by which point there was nothing left to forecast; there was only wreckage to describe.

This is not a gauge that warns you. It is a gauge that confirms, long after the fact, what the price action has already told everyone. It reads low going in and screams at the bottom. And here is the part that should stop the conversation cold: look at the right-hand edge of that chart. After the 2020 spike, concern climbed through 2023 and 2024, pushed toward 40% in 2025 - the highest sustained reading since 2008 - and then, in the most recent prints, rolled over and fell back toward 5–6%.

Five percent. In June 2026. The same reading it gave in December 2007, when the recession had already begun.

Investor concern is not a measure of risk. It is a measure of what investors have noticed. Those are not the same thing, and the gap between them is where fortunes are made and lost.

So when an apparently senior figure in this industry tells me he will pay attention “when concerns become more acute,” he is telling me - without realising it - that he intends to notice the recession at roughly the moment it becomes undeniable to everyone else. Which is to say: a year late. I do not say that as an insult. I say it because it is documented. This particular gentleman was wrong in 2019, and wrong again in 2022, in his own published analyses. The pattern is not hidden. It is on the record.

III. Why they keep missing it

The obvious question is: how? How does an entire, enormously well-resourced, deeply credentialed industry keep standing in the same spot every cycle and getting hit by the same bus? I have come to believe it comes down to three things, and none of them is stupidity.

Sentiment. Nobody wants to be the person talking about the coming downturn while the stock market is making new highs and everyone at the dinner table is up thirty percent. It is socially and professionally expensive to be early and bearish. So the incentive is to look away.

Laziness. And I mean this precisely, not as a slur: after each miss, almost nobody does the forensic work of asking why they were wrong. So, they reach for the same analytical toolkit next time - the same lagging indicators, the same coincident dashboards - and they get the same result. A method that failed in 2008 and failed in 2022 is still, remarkably, the house method.

A thin grasp of dynamics. This is the deep one. Most of the industry does not have a working model of what actually leads what in an economy. They watch outputs and call them causes. They read a calm concern-gauge and conclude the economy is calm. They are, in the most literal sense, looking at the wrong hand.

Good thing these are not the people landing rockets. An engineer this wrong about which variable leads would not get a polite “follow up later in the year.” The vehicle would be in the ocean.

IV. A recession is not a shock. It is a rollover.

Here is the thing the crowd gets fundamentally backwards, and it is worth slowing down for, because everything downstream depends on it.

Most people believe a recession is caused by an event. A shock. Lehman Brothers fell over, and therefore 2008. But that is the story told backwards. Lehman did not cause the recession. The recession - the underlying rollover already in motion - created the toxic environment in which a Lehman becomes possible. The consumer was already pulling back. Unemployment was already rising. That is what turned a pile of mortgages into a pile of bad loans, not the other way around.

A recession begins for one reason above all others. The consumer - who is roughly 70% of GDP through private consumption - starts to hurt. And when households begin to face hardship, they hold back. That is the whole engine. Demand softens, so businesses need fewer people, so hiring slows, so more households grow cautious, so demand softens further. A feedback loop. The economy does not get struck by lightning. It rolls over, slowly and then all at once, under its own weakening weight.

The magician shows you the loud hand - IPOs, the AI build-out, endless data-centre demand, a melting-up index - while the quiet hand, the consumer, does the actual work of turning the cycle.

All of that loud-hand material is wonderful for conversation. It is nearly useless for timing a recession. If you want to know when the cycle turns, you do not watch the fireworks. You watch the consumer, the labour market, and the feedback loop between them. So let us do exactly that - and let us keep asking, at every chart, the question the gatekeeper never asks: what is the most probable scenario here?